In this article we outline the basic elements of blockchain infrastructure and analyze the challenges they're facing.

Node Infrastructure (MC – US$10B-50B)

The bulk of the market share is represented by Infura (Consensys) and Alchemy. Due to their centralized nature, if any of these node providers were to encounter a fault or accident, the entire blockchain would suffer downtime. In response, decentralized node providers such as Pocket Network have emerged, although their market share remains small.

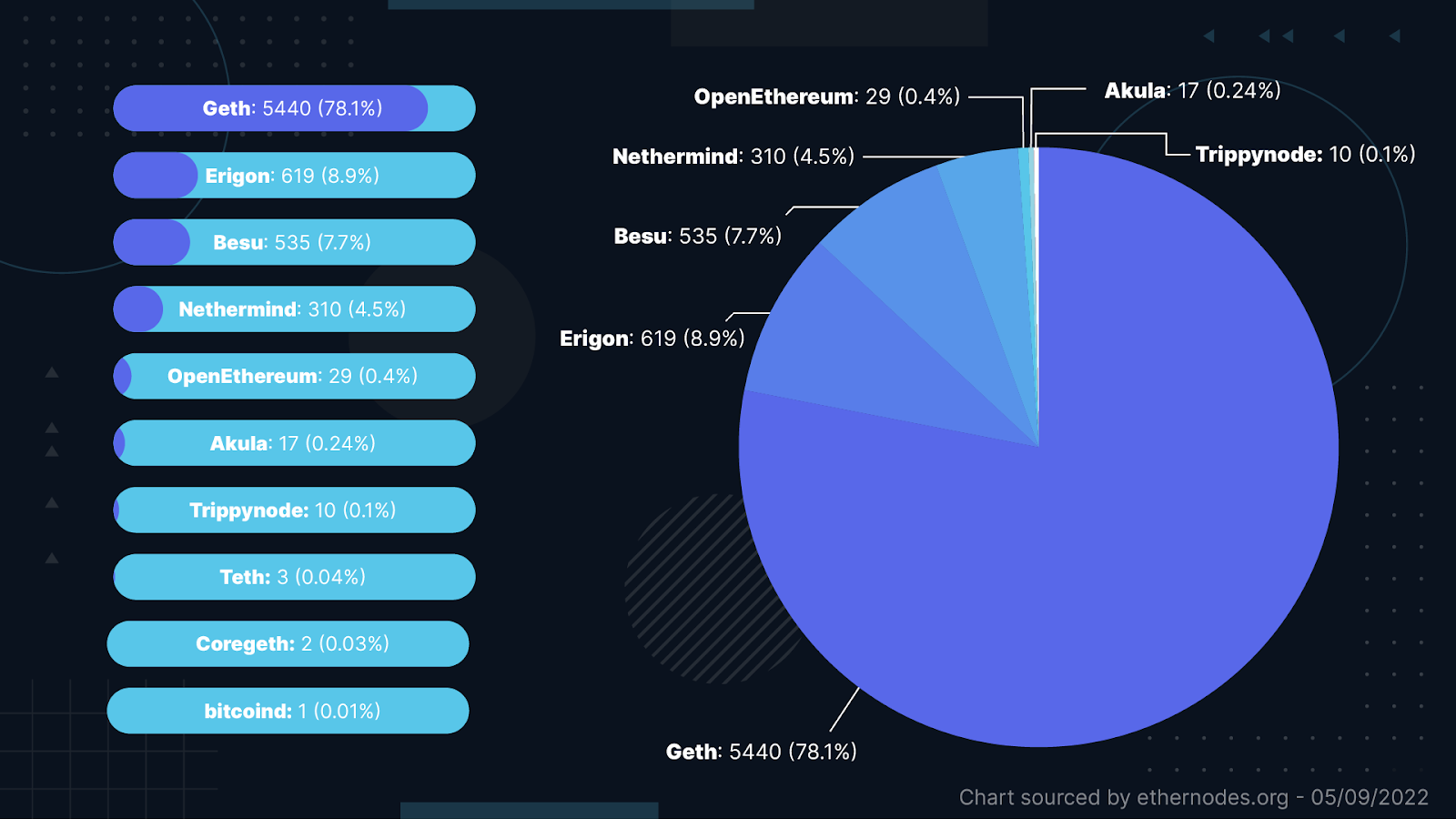

Most Eyjerum Hosted Nodes are run by the node infrastructure providers with Geth, which is the Ethereum Client. Hence, it's all masked under Geth.

Decentralized node providers are becoming increasingly relevant if we take into account that businesses such as Infura and Alchemy usually depend on a single cloud provider. This poses a high risk for the network as nodes are centralized on the servers of a few major companies. In fact, 69% of the 65% of Ethereum nodes hosted in data centers are distributed among three providers.

Running on a centralized infrastructure exposes networks to censorship and service interruptions. Hypothetically, if Ethereum nodes were not to comply with government regulations, AWS could be required to stop hosting them and 33% of the network would go offline.

Oracles (MC – US$5B-10B)

In the past, Blockchain Oracles were dominated by Chainlink, with a fair share of issues regarding trust and unnecessary costs. First-party oracles, represented by API3, emerged in the market to address some of these problems.

First-party oracles are operated by the Application Programming Interface (API) providers themselves. In contrast, Chainlink and similar solutions employ third-party oracles to build this interface, which has led to the Oracle Problem: a conflict between security, authenticity, and trust for the trustless execution of smart contracts. As a consequence, neither the protocol nor the node is optimized to be operated by API providers, because API providers are not even in the picture, which harms the feasibility of first-party oracles.

Storage (MC – US$1B-5B)

The IPFS protocol is heavily used in the industry, but it has its own shortcomings. It has difficulty being objective about what the confirmation standard of real data is in the verification process by Filecoin, which is aimed at deterring the storing of junk data by miners. This is part of the reason decentralized storage projects such as Arweave appeared in the market.

Since Arweave is still unable to guarantee privacy, the market is pivoting to new storage projects with Share-2-Earn models and Baidu Cloud, which has released a range of web3 products to better cater to current web3 developments.

Security Audit (MC – US$1B-5B)

Although Certik has the highest market share in this sector, there has been an increasing amount of negative feedback. As a result, security audit vendors such as Slow Fog, Chain Security, and Blocksec have seen rapid growth over the last year.

Wallets (MC – US$1B-5B)

Metamask remains the leading wallet provider. Competitors can only aim at gaining traction by offering products that are easier to use or by reducing the barrier to entry. Some offerings currently in the market include non-EVM-compatible chains, cross-chain compatibility, on-ramp and off-ramp, NFT trading, and eliminating the risk of lost seed phrases by introducing new mechanisms.

For custodial and wallets, an example of these mechanisms is having a centralized party to safekeep the seed phase for users. In the case of social wallets, users can initiate a transaction to generate a new private key and, if more than 50% of the user-appointed guardians sign it, the wallet would be recovered. Still, this sector is currently saturated and difficult to penetrate into.

While there are one or more decentralized players in each of the layers in the infrastructure stack, most are still Proofs of Concept and not production-ready. These are the most technically challenging problems to fix, but decentralizing the infrastructure is essential to drive mass adoption and, after all, an application is only as decentralized as its most centralized layer.

Note: All market cap figures in this article are estimated based on the key players' valuations during their last round of fundraising.

About Polkastarter

Polkastarter is the leading decentralized fundraising platform enabling crypto’s most innovative projects to kick start their journey and grow their communities. Polkastarter allows its users to make research-based decisions to participate in high-potential IDOs, NFT sales, and Gaming projects.

Polkastarter aims to be a multi-chain platform and currently, users can participate in IDOs and NFT sales on Ethereum, BNB Chain, Polygon, Celo, and Avalanche, with many more to come.